BY DATUK PROF M NASIR SHAMSUDIN

TRENDS in Malaysian food consumption are typical of those of developing economies, where structural changes in dietary habits can be categorised into the following stages: an initial increase in the consumption of traditional staple foods (such as rice); followed by an increase in the consumption of non-traditional staple foods (such as wheat and secondary products derived from traditional staple material); diversification in consumption habits including the time and place of consumption; and an increase in the consumption of a greater variety and volume of higher value and higher proteins foods (such as meat, fish and milk).

The latter is likely to be at the expense of traditional sources of lower-quality protein (such as cereals) rather than the sources of traditional higher-quality protein. Hence, in Malaysia, it is generally observed that the demand for meat, fish, dairy products, and food away from home has increased considerably, while the importance of rice as a staple food is decreasing steadily.

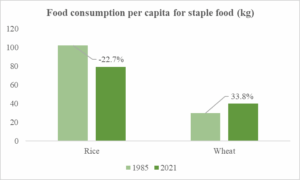

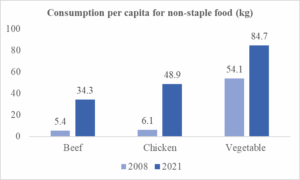

For example, from 1985 – 2021, per capita rice consumption declined by 22.7%, from 102.2 to 79 kg. Wheat consumption, a substitute for rice, has increased by 33.8%, from 29.9 to 40 kg over the same period. Consumption of beef and chicken, from 2008 to 2021, has increased from 5.4 kg and 34.3 kg to 6.1 kg and 48.9 kg, respectively. Per capita vegetable consumption has increased from 54.1 kg in 2008 to 84.7 kg in 2021. Thus substitution of calories obtained from non-staples for staple food sources has been substantial.

Consumers also demand new food products, new packaging, more convenience, new delivery systems, and safer and more nutritious foods. The future food choices will have implications for the organizational structure of the agri-food industry and for the economic well-being of farmers, food processors, retailers, and other participants in the food production and marketing system.

There are several concerns that need to be addressed with the changes in the consumption patterns that created a demand-pull inflation. One is the price of some of the foods, like meat and fish, which have been on the rise over the recent past.

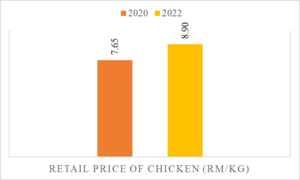

For instance, the retail price of chicken increased from RM7.65/kg in March 2020 to RM8.90 in March 2022, an increase of 16.3%. Although Malaysia’s inflation in May 2023 was at 2.8%, food inflation was at 5.9%. This has been a major point of contention by consumers, and despite efforts to regulate or even control their prices; these have not been entirely successful.

These constitute impediments to economic access by the consumers. Much more concern is related to the aspect of availability and stability.

With the changes in food demand, Malaysia has become increasingly reliant on imports to meet the growing demand for meats and several fruits and vegetables.

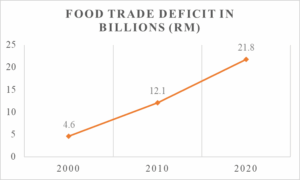

As a consequence of greater food import dependency, Malaysia has been recording more significant food trade deficits over the years, from RM4.9 billion in 2000 to RM12.1 billion in 2010 to RM21.8 billion in 2020.

Economic growth is the main driver for such changes in the food consumption pattern. An increase in per capita income has pushed up middle-class consumers’ purchasing power which generated rising demand for food and shifted food demand away from traditional staples and towards higher-value foods and changes in the market for food attributes.

As income levels have grown, Malaysian consumers are also willing to pay for the quality.

For a country that is undergoing rapid structural transformation and urbanisation, changes in tastes and lifestyles, market development, and occupation have also influenced the food demand. Thus understanding the changes in food consumption patterns will provide one of the best bases for adding value to the food supply chain to meet the consumer needs and for appropriate policy formulation.

From a marketing standpoint, a value creation and delivery sequence of a food product approach is the way forward to seize opportunities from changes in food consumption patterns. The value creation in a food product starts with the customisation in value for specific consumer segments, markets, and value positioning.

After choosing the value, it is the stage of providing the value. The power of this stage is the value-adding potential in each element of the food product when it is viewed from a broader and more holistic business perspective, besides, special attention given to the targeted segment demand and expectations.

A proactive sales force, creative promotions, and catchy advertising then kick in to communicate the value to the targeted segment. This will offer the basis for a firm to create and deliver value by leveraging on inherent elements and the potential of penetrating the consumer market.

Moving forward, an aligned market-led supply chain is proclaimed to move away from traditional open market coordination. The functions of the aligned market-led supply chain are to offer differentiated and complex food products, which explicitly specify the value-creating activities in the production-distribution process and provide an explicit structure for the linkages among these activities or processes.

These will require mutual contribution from various supply players such as input suppliers, producers, processors, marketers, and retailers in order to share market information.

In conceiving the information of demanded food product attributes, the Malaysian agri-food supply chain players must adopt a value creation and delivery approach to capture the value before it decays.

The basic principle is to produce or provide a product or service that has sufficient value for customers or end-users that they are willing to pay for. However, a more discerning and clear vision is needed for specifying consumer-desired product attributes individually.

In particular, the vision should articulate how the Malaysian agri-food players can respond appropriately to the changes in consumer demand and expectations in order to capture the best profit margins under different economic climates.

From an agri-food policy perspective, it must consider both agricultural and health sectors, thereby enabling the development of coherent and sustainable policies that will ultimately benefit agriculture, human health, and the environment.

Note: The author is an agricultural economics analyst in the Faculty of Agriculture, Universiti Putra Malaysia. He is also a member of the National Agriculture Advisory Council, the Ministry of Agriculture, and the Food Industry.